ASK MAT – Do you think the JFSC should revisit and update its three-tier test for beneficial ownership and controllers

18/02/2026

ASK MAT –

- Do you think the JFSC should revisit and update its three-tier test for beneficial ownership and controllers?

- I ask this because, after attending a Comsure sanctions briefing,

- I understand that the question of "control" has become more pronounced with the expansion of UK sanctions regimes, especially since 2022, in response to global events such as the Russia-Ukraine conflict. In these contexts, complex corporate structures are commonly used to obscure ownership and evade sanctions.

- Furthermore, I understand that the UK Office of Financial Sanctions Implementation (OFSI), part of HM Treasury, has identified issues with the current ownership and control test under Regulation 7(4) of the Russia (Sanctions) (EU Exit) Regulations 2019, particularly in its practical application.

- From the latest Comsure briefing, I understood

- OFSI suggests that the Regulation 7 test:

- Lacks sufficient clarity, effectiveness, and proportionality, leading to challenges for businesses and compliance teams in implementing sanctions without undue burden.

- Creates a key problematic area in "hypothetical control," where control is assessed based on the potential influence that a sanctioned person could exercise, even if they are not currently doing so.

- Generates uncertainty, as it requires firms to speculate on scenarios that may not be evident from public records or standard due diligence.

- Furthermore, UK case law has refined the Regulation 7 test,

- Effectively creating a four-tier typology, unlike the three-tier approach in existing guidance.

- And in response to the above matters, the OFSI:

- Is calling for evidence, which opened on February 16, 2026, and remains open until 11:59 p.m. on April 13, 2026. This aims to gather input from industry stakeholders (e.g., financial institutions, law firms, and businesses) on the challenges they face.

- Wishes to evaluate whether the current test strikes the right balance: maintaining robust enforcement against sanctioned targets while ensuring regulations are workable and do not unduly hinder legitimate economic activity.

Mat's Response

- Thank you for your insightful question and for demonstrating a keen interest in the briefing. It highlights the interplay between regulatory rules and best practices, particularly with respect to the responsibilities of regulated Jersey firms under the relevant frameworks.

- In my view, yes, the JFSC should revisit and update its three-tier test to incorporate elements of the UK four-tier typology, particularly for sanctions compliance.

- While the current guidance is sufficient for core AML/CTF/CPF obligations, and the upcoming enhancements will strengthen it, the four-tier judicial precision better addresses hypothetical and de facto control in sanctions contexts, reducing overreach and enhancing evasion detection.

- Given Jersey's statutory alignment with UK sanctions and the persuasive nature of UK case law, integrating the four-tier would promote consistency and legal certainty.

- The JFSC should monitor the outcomes of the UK call for evidence (expected post-April 2026) and consider further amendments following the May 31, 2026, Handbook implementation, potentially through targeted consultations on sanctions-specific ownership and control.

To explain my rationale and thinking, and build on the Comsure training you received, I will provide the following briefing.

MATS briefing

- This briefing examines whether the Jersey Financial Services Commission (JFSC) should revisit and update its three-tier test for identifying beneficial owners and controllers, in light of Jersey's obligations to comply with UK sanctions and recent UK case law establishing a four-tier typology of control.

- Jersey's alignment with UK sanctions regimes, combined with evolving judicial interpretations in the UK, raises questions about the adequacy of the current JFSC guidance for comprehensive compliance, particularly where AML/CTF/CPF and sanctions overlap.

- The analysis draws on JFSC guidance, UK developments, and recent updates to assess the need for changes.

Jersey's Obligations Under UK Sanctions

- Jersey implements UN and autonomous UK sanctions through the Sanctions and Asset-Freezing (Jersey) Law 2019 (SAFL) and the Sanctions and Asset-Freezing (Implementation of External Sanctions) (Jersey) Order 2021 [1].

- This framework aligns with the UK's Sanctions and Money Laundering Act 2018 (SAMLA), meaning UK concepts of "ownership and control" – such as under Regulation 7(4) of the Russia (Sanctions) (EU Exit) Regulations 2019 – apply similarly in Jersey.

- While JFSC's three-tier test primarily supports AML/CTF/CPF under the Money Laundering (Jersey) Order 2008, it indirectly aids sanctions compliance by identifying UBOs/controllers for screening against lists like the UNSC Consolidated List or UK OFSI lists.

- However, sanctions require a broader assessment of control to prevent evasion, and Jersey courts may consider UK judgments persuasive, though none have yet adopted UK refinements.

Current JFSC Guidance on the Three-Tier Test

- The JFSC’s Beneficial Ownership and Controller Guidance [2] and AML/CFT/CPF Handbook (Section 4) [3] outline the three-tier test, derived from FATF standards, as a sequential, risk-based framework to identify natural persons with ultimate ownership or control:

- Tier 1: Natural persons with material controlling ownership interest (e.g., ≥25% in lower-risk cases, direct/indirect voting rights, or via agreements like shareholders’ agreements).

- Tier 2: Persons exercising ultimate effective control through non-ownership means (e.g., personal connections, financing, family influence, historical associations).

- Tier 3: Senior managing officials if Tiers 1-2 are unclear.

- This test applies to entities like companies, trusts, and partnerships, emphasising evidence collection and risk adjustment.

- It is accurate and comprehensive for AML/CTF/CPF, embedding proliferation risks and ensuring identification in complex structures.

- However, it is not directly tailored for sanctions, focusing on beneficial ownership rather than the broader "control" under sanctions law.

- Recent JFSC consultations and feedback indicate updates to the Handbook effective May 31, 2026, included:-

- Enhancements to Section 4.6 on "control through other means" (making Tier 2 mandatory),

- Refined illustrative examples (e.g., family heads, lenders' exercisable control, trust enforcers/protectors), and

- Alignment with FATF and UK registry guidance on significant influence [4].

- These changes address complex structures but do not alter the three-tier structure or incorporate sanctions-specific tests like the UK four-tier typology as discussed in the next section.

UK Developments: The Four-Tier Typology and Ongoing Consultation

- Recent UK case law has refined the "control" test under sanctions regulations.

- The 2024 High Court judgment in Kevin Hellard & Ors v OJSC Rossiysky Kredit Bank & Ors [2024] EWHC 1783 (Ch) [5] introduced a four-tier typology to reconcile broader (Mints v PJSC National Bank Trust [2023] EWCA Civ 1132) [6] and narrower (Litasco SA v Der Mond Oil and Gas Africa SA [2023] EWHC 2866 (Comm)) [7] interpretations:

- De jure control: Absolute legal rights (e.g., veto powers in constitutions).

- Actual present de facto control: Practical influence without legal rights (e.g., coercion).

- Potential future de jure control: Legal means to obtain control (e.g., options to acquire shares).

- Potential future de facto control: Rare, realistic non-legal influence without penalties or cooperation needs.

- This framework emphasises plausible potential control to target evasion without overreach.

AVOID ABSURD OUTCOMES

- The four-tier offers greater precision and clarity, better detecting evasion while avoiding absurd outcomes (e.g., per Secretary of State for Work and Pensions v Johnson [2020] EWCA Civ 778) [9].

- The Secretary of State for Work and Pensions v Johnson [2020] EWCA Civ 778 case serves as a key analogy in discussions of UK regulatory frameworks, including the ownership and control test in financial sanctions, to illustrate the administrative law principle of irrationality.

- In Johnson, the Court of Appeal ruled that the Universal Credit regulations' method for calculating earned income was irrational and unlawful when two monthly salary payments fell into a single assessment period due to non-working days (e.g., weekends or bank holidays shifting pay dates).

- This "double payment" scenario led to claimants losing entitlement to benefits or facing significant reductions in support, creating foreseeable and anomalous outcomes that undermined the policy's intent to encourage work without imposing undue hardship.

- The court emphasised that while the threshold for irrationality is high, regulations must be interpreted or adjusted to avoid disproportionate or absurd results that frustrate their core objectives.

- In the context of OFSI's ownership and control test, Johnson fits as a comparative precedent for critiquing overly broad or speculative interpretations (e.g., hypothetical control scenarios) that could lead to similar absurdities, such as inadvertently sanctioning vast swathes of an economy or unrelated entities based on tenuous links.

- This aligns with judicial cautions in sanctions cases like Mints v PJSC National Bank Trust [2023] EWCA Civ 1132, where expansive control definitions were rejected to prevent illogical extensions.

- Proponents of the four-tier typology (from Hellard v OJSC Rossiysky Kredit Bank [2024] EWHC 1573 (Ch)) invoke Johnson to argue that a more structured, evidence-based approach better balances enforcement goals with practicality, minimising de-risking and compliance burdens while detecting evasion, much like how the DWP was compelled to amend Universal Credit rules post-Johnson to address the anomaly.

HYPOTHETICAL CASE

- In the following hypothetical case (e.g., a designated person retaining unexercised director nomination rights post-share transfer), the four-tier pinpoints potential de jure control more tightly than the three-tier's indirect/personal categories.

Hypothetical Case Study: Application of Control Tests to a Designated Person's Latent Rights

- Scenario Setup:

- Person A is a Designated Person (DP) under the Russia (Sanctions) (EU Exit) Regulations 2019.

- Before their designation, Person A founded and owned Company X.

- After designation, Person A transfers all their shares in Company X to three associates (Persons B, C, and D) and resigns as director and signatory.

- Public filings show only Persons B, C, and D as shareholders and directors.

- Day-to-day decisions appear to be taken by the board without reference to Person A, and there is no evidence that Person A is currently exercising control.

- Key Latent Element:

- However, before designation, the shareholders executed a deed that remains in force, granting Person A the right exercisable at any time by written notice to nominate and remove a majority of the directors.

- These rights have not been exercised since designation, and no board changes have been made at Person A’s behest.

- Analysis and Implications:

- Although there is no evidence that Person A is currently exercising control, there is good reason to believe that Person A could, if they chose to do so, exercise control in most cases or in significant respects by using these existing legal rights to appoint directors.

- If an entity meets this test (i.e., is deemed controlled by the DP), its assets should be frozen, and dealings with it are prohibited, extending the reach of sanctions beyond the directly sanctioned individual.

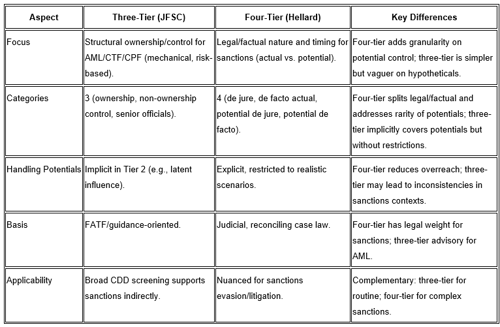

Comparison of Three-Tier and Four-Tier Typologies

- How the Tests Apply

- Under the Three-Tier Test:

- This scenario fits primarily as indirect control (via proxies/associates and obscured structure), with possible personal elements (associates implying relationships).

- Direct control is absent post-transfer. It highlights the "ability" to influence but does not sharply distinguish between actual and potential control.

- Under the Four-Tier Test:

- This aligns with potential future de jure control; the deed provides a legal means (enforceable right) to obtain control over the board, even if unexercised. It's not actual de jure (not embedded in Company X's constitution) or de facto (no current "calling the shots").

- Potential de facto control is unlikely, as it relies on legal rights rather than mere influence.

- The four-tiered strict test supports the conclusion (a good reason to suspect control via existing rights) without overextending to implausible scenarios.

- This case study illustrates the comparative strengths of the four-tier typology in providing a "tighter fit" for hypothetical or latent control situations, as per the details in the ask Mat question.

OFSI

- As of February 18, 2026, HM Treasury and OFSI's call for evidence on the ownership and control test remains open (published February 16, 2026; closes April 13, 2026), seeking views on typologies like the four-tier, without interim outcomes [8].

- No Jersey-specific adoption of the four-tier has occurred.

Implications for Jersey

- Jersey's sanctions alignment with the UK necessitates robust control assessments to prevent evasion.

- The JFSC three-tier effectively supports AML/CTF/CPF but lacks the four-tier's sanctions-specific nuances, potentially leading to inconsistencies.

- Upcoming Handbook updates (May 31, 2026) enhance Tier 2 and complex structures but do not integrate the four-tier or reference Hellard [4].

- Firms currently complement the three-tier with a four-tier for sanctions. Still, formal JFSC adoption could improve consistency, especially amid UK policy evolution (e.g., the withdrawal of Mints' Supreme Court appeal in May 2025) [10].

Conclusion: Are Changes to JFSC Guidance Needed?

- In consideration of the above analysis, yes, the JFSC should revisit and update its three-tier test to incorporate elements of the UK four-tier typology, particularly for sanctions compliance.

- While the current guidance is sufficient for core AML/CTF/CPF and upcoming enhancements strengthen it, the four-tier judicial precision better addresses hypothetical and de facto control in sanctions contexts, reducing overreach and enhancing evasion detection.

- Given Jersey's statutory alignment with UK sanctions and the persuasive nature of UK case law, integrating the four-tier would promote consistency and legal certainty.

- The JFSC should monitor the UK call for evidence outcomes (post-April 2026) and consider further amendments after the May 31, 2026, Handbook implementation, potentially through targeted consultations on sanctions-specific ownership/control.

Web Sources Used

[1] Sanctions and Asset-Freezing (Jersey) Law 2019 and Related Orders - https://www.gov.je/Industry/Finance/FinancialCrime/Sanctions/pages/internationalsanctions.aspx

[2] JFSC Beneficial Ownership and Controller Guidance - https://www.jerseyfsc.org/industry/guidance-and-policy/beneficial-ownership-and-controller-guidance/

[3] JFSC AML/CFT/CPF Handbook (Sections 1-18) - https://www.jerseyfsc.org/media/e1ldlytw/use-to-amend-20230831-hb-consolidated-sections-1-18-track-01072024-23012025.pdf

[4] Feedback on Enhancements to the AML/CFT/CPF Handbook - https://www.jerseyfsc.org/media/bzlk5pio/feedback-on-enhancements-to-the-aml-cft-cpf-handbook.pdf

[5] Kevin Hellard & Ors v OJSC Rossiysky Kredit Bank & Ors [2024] EWHC 1783 (Ch) - https://www.rahmanravelli.co.uk/assets/Uploads/2ef5ed6698/Kevin-Hellard-Ors-v-OJSC-Rossiysky-Kredit-Bank-in-liquidation-Ors-v3.pdf

[6] Mints v PJSC National Bank Trust [2023] EWCA Civ 1132 - https://www.judiciary.uk/wp-content/uploads/2023/10/Mints-v-PJSC-judgment-061023.pdf (also available at https://www.bailii.org/ew/cases/EWCA/Civ/2023/1132.html)

[7] Litasco SA v Der Mond Oil and Gas Africa SA [2023] EWHC 2866 (Comm) - https://www.bailii.org/ew/cases/EWHC/Comm/2023/2866.html

[8] HM Treasury and OFSI Call for Evidence on Ownership and Control Test in UK Financial Sanctions Regulations (February 2026) - https://www.gov.uk/government/calls-for-evidence/ownership-and-control-test-in-uk-financial-sanctions-regulations

[9] Secretary of State for Work and Pensions v Johnson [2020] EWCA Civ 778 - https://www.bailii.org/ew/cases/EWCA/Civ/2020/778.html

[10] Mints v PJSC National Bank Trust Supreme Court Appeal Withdrawn (May 2025) - https://supremecourt.uk/cases/uksc-2023-0146

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.