ASK MAT:- I have had my annual AML/CTF/CPF training, and I’m confused between subjective and objective suspicion

09/04/2025

MAT SAYS: Thank you for a great question. Many people get confused with this area, so many “external SARs/STRs [eSAR]” are based on bias and/or defensive motivations rather than suspicion grounded in observable and verifiable facts or evidence. They are impartial and not influenced by personal feelings, biases, or fear.

In Jersey, the JFSC try to help with these issues by providing the following guidance.

Although helpful, I think the above could benefit from more explanation.

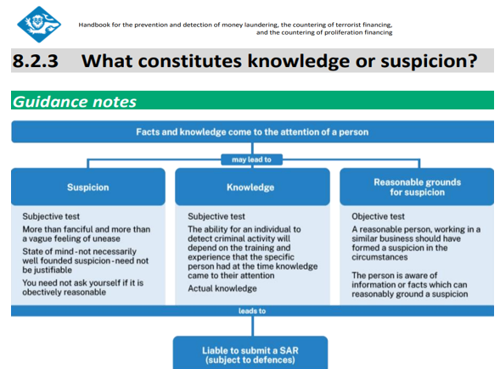

The difference between subjective and objective suspicion lies in the basis and perspective from which the suspicion arises:

- Subjective Suspicion:

- Based on Personal Belief: It arises from an individual's feelings, beliefs, or opinions.

- Influenced by Personal Bias: The individual's experiences, emotions, and biases shape the suspicion.

- Example: A police officer suspects someone because they "feel" the person looks suspicious, without concrete evidence.

- Objective Suspicion:

- Based on Verifiable Facts: It is grounded in observable and verifiable facts or evidence.

- Unbiased and Impartial: The suspicion is not influenced by personal feelings or biases.

- Example: A police officer suspects someone because they match the description of a suspect in a recent crime, supported by evidence.

iSAR to eSAR

- Considering the above examples and explanations, the work of the MLRO/Nominated officer is vital. Their job is to analyse all iSARs to ensure personal feelings or biases do not influence the report.

- The MLRO is looking for information that is grounded, observable, verifiable, and, most importantly, useful to the FIU to prevent and detect financial crime.

- In legal contexts, objective suspicion is often preferred because it relies on factual evidence rather than personal judgment.

IMPORTANT DISTINCTIONS

- In the context of financial crime reporting within the Suspicious Activity Report (SAR) and Suspicious Transaction Report (STR) regimes, the implications of subjective and objective suspicion are significant:

Subjective Suspicion

- Personal Judgment: Financial institutions may rely on the personal judgment of their employees to identify suspicious activities. This can lead to inconsistencies, as individuals may have varying thresholds for what they consider suspicious.

- Potential for Bias: Personal biases can influence subjective suspicion, which might result in either over-reporting or under-reporting of suspicious activities.

- Training and Awareness: Institutions must invest in extensive training to ensure that employees can recognise and report suspicious activities effectively, despite the subjective nature of their judgments.

Objective Suspicion

- Standardised Criteria: Objective suspicion relies on standardised criteria and verifiable facts, leading to more consistent and reliable reporting.

- Reduced Bias: By focusing on observable evidence, objective suspicion minimises the influence of personal biases, ensuring that reports are based on concrete indicators of suspicious activity.

- Regulatory Compliance: Objective suspicion aligns more closely with regulatory expectations, providing a clear, evidence-based rationale for reporting, which is crucial for compliance with anti-money laundering (AML) regulations.

Implications for SAR/STR Regimes

- Effectiveness: Objective suspicion enhances the effectiveness of SAR/STR regimes by ensuring that reports are based on solid evidence, making them more useful for law enforcement and regulatory bodies.

- Resource Allocation: Financial institutions can allocate resources more efficiently by focusing on activities that meet objective criteria rather than relying on subjective judgments that may vary widely.

- Legal Protection: Reports based on objective suspicion are more defensible in legal contexts, as verifiable facts rather than personal opinions support them.

While both types of suspicion are involved in financial crime reporting, objective suspicion is generally preferred for its consistency, reliability, and alignment with legal and regulatory expectations.

Closing thought

The above matters are critical to iron out in any employee training—if you want to know more, please get in touch with the Comsure team or me directly [mathew@comsuregroup.com] if you're going to organise additional training to what you have had so far.

If you want to read more about the above thoughts, please review the following sources.

- "Subjective" vs. "Objective": What's The Difference? https://www.dictionary.com/e/subjective-vs-objective/

- Difference Between Objective and Subjective (with Comparison Chart ... www.keydifferences.com/difference-between-objective-and-subjective.html

- Subjective Test vs Objective Test - UOLLB First Class Law Notes® https://uollb.com/blogs/uol/subjective-test-vs-objective-test

- Answers to Frequently Asked Questions Regarding Suspicious Activity ... www.fincen.gov/sites/default/files/2021-01/Joint SAR FAQs Final 508.pdf

- Suspicious Activity Reporting — Overview https://bsaaml.ffiec.gov/docs/manual/06_AssessingComplianceWithBSARegulatoryRequirements/04.pdf

- Connecting the Dots…The Importance of Timely and Effective ... - FDIC - https://www.fdic.gov/bank-examinations/connecting-dotsthe-importance-timely-and-effective-suspicious-activity-reports

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.