Decoding the UK's Sanction Ownership and Control Test: Challenges, Hypotheticals, and the Push for Reform

18/02/2026

Understanding “CONTROL” has become more pronounced with the expansion of UK sanctions regimes, especially since 2022, in response to global events such as the Russia-Ukraine conflict, where complex corporate structures are common to obscure ownership.

The UK Office of Financial Sanctions Implementation (OFSI), part of HM Treasury, has

- Identified issues with the current ownership and control test (Regulation 7 of the Russia (Sanctions) (EU Exit) Regulations 2019), particularly in its practical application.

OFSI suggested the Regulation 7 test

- Lacks sufficient clarity, effectiveness, and proportionality, leading to challenges for businesses and compliance teams in implementing sanctions without undue burden.

- Creates a key problematic area is "hypothetical control," where control is assessed based on the potential influence that a sanctioned person could exercise, even if they are not currently doing so.

- Creates uncertainty, as it requires firms to speculate on scenarios that may not be evident from public records or standard due diligence.

In response, the OFSI:-

- Is calling for evidence, open until 13 April 2026, and aims to gather input from industry stakeholders (e.g., financial institutions, legal firms, and businesses) on the challenges of

- Wishes to evaluate whether the current test strikes the right balance: maintaining tough enforcement against sanctioned targets while ensuring regulations are workable and do not unduly hinder legitimate economic activity.

Responses will inform potential reforms to make the test clearer, more effective, and proportionate, possibly through updated guidance, legal definitions, or examples.

OVERVIEW OF THE OWNERSHIP AND CONTROL TEST

- In UK financial sanctions regulations, the "ownership and control" test is a critical mechanism used to determine whether an entity (such as a company or organisation) is subject to sanctions because it is owned or controlled by a designated (sanctioned) person.

- Ownership is typically straightforward, often defined by holding more than 50% of shares or voting rights.

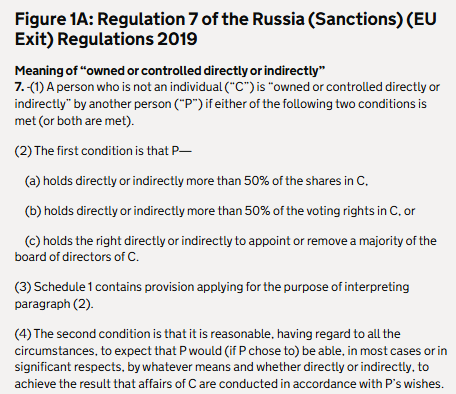

MEANING OF “OWNED OR CONTROLLED DIRECTLY OR INDIRECTLY” [ALSO SEE FIG 1A BELOW]

- Regulation 7 of the Russia (Sanctions) (EU Exit) Regulations 2019 - states

- An entity is owned or controlled directly or indirectly by another person in any of the following circumstances:

- The person holds (directly or indirectly) more than 50% of the shares or voting rights in an entity.

- The person has the right (directly or indirectly) to appoint or remove a majority of the board of directors of the entity.

- It is reasonable, having regard to all the circumstances, to expect that a DESIGNATED PERSON [DP] would (if they chose to) be able, in most cases or significant respects, by whatever means and whether directly or indirectly, to achieve the result that affairs of an entity are conducted in accordance with that DP’s wishes.

Below are the current measures of control

THREE-TIER CONTROL

There are various ways to structure or exercise control.

- Control is broader and can include the ability to direct or influence the entity's activities, even without formal ownership.

Some simple examples of types of control include:

- 1 - Direct control:

- This could arise where a DP holds a majority voting right in an entity, allowing them to make decisions directly.

- 2 - Indirect control:

- In these cases, a DP might exert influence through a proxy or intermediary or via a complex ownership structure, making the link between the DP and the entity less obvious.

- 3 - Personal control:

- Here, a DP could influence the affairs of an entity by exercising control through personal or familial relationships rather than through formal legal rights or contractual powers.

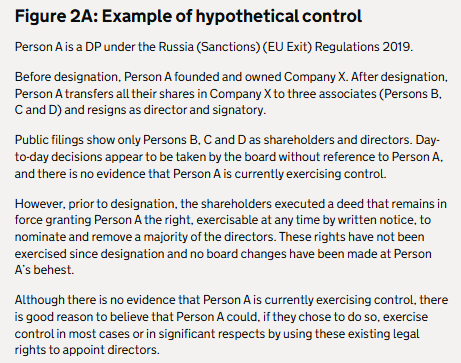

Example Hypothetical Case Study

- A worked example of what hypothetical control might look like in practice [also see Figure 2A: Example of hypothetical control below]

- Person A is a DP under the Russia (Sanctions) (EU Exit) Regulations 2019.

- Before designation, Person A founded and owned Company X.

- After designation, Person A transfers all their shares in Company X to three associates (Persons B, C and D) and resigns as director and signatory.

- Public filings show only Persons B, C and D as shareholders and directors.

- Day-to-day decisions appear to be taken by the board

- Without reference to Person A, and

- There is no evidence that Person A is currently exercising control.

- However, before designation, the shareholders executed a deed that remains in force,

- Granting Person A the right, exercisable at any time by written notice,

- To nominate and remove a majority of the directors.

- These rights have not been exercised since designation, and no board changes have been made at Person A’s behest.

- Although there is no evidence that Person A is currently exercising control,

- There is a good reason to believe that Person A could, if they chose to do so, exercise control in most cases or in significant respects by using these existing legal rights to appoint directors.

- If an entity meets this test,

- Its assets are [SHOULD BE] frozen, and

- Dealings with it are prohibited,

- and as a result,

- extending the reach of sanctions beyond the directly sanctioned individual.

3 GOES INTO 4 - DE JURE AND DE FACTO ROUTES TO CONTROL.

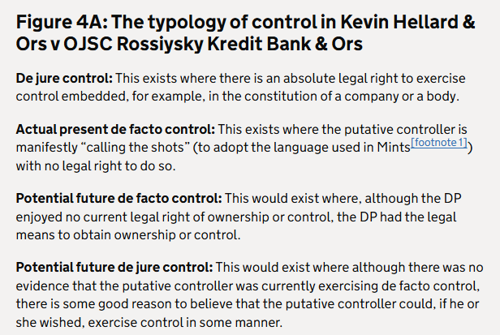

- In recent years, English courts have considered the interpretation of the control test in several judgments. For example, in June 2024, Deputy Judge Nicholas Thompsell ruled on the case of Kevin Hellard & Ors v OJSC Rossiysky Kredit Bank & Ors.

- In this judgment, Mr Justice Thompsell introduced a typology of control, organising the concept of control in the control test into four categories. These are set out here

4 TIER TEST

- The typology of control in Kevin Hellard & Ors v OJSC Rossiysky Kredit Bank & Ors [See below Figure 4A: The typology of control]

- De jure control:

- This exists where there is an absolute legal right to exercise control embedded, for example, in the constitution of a company or a body.

- Actual present de facto control:

- This exists where the putative controller is manifestly “calling the shots” (to adopt the language used in Mints[footnote 1]) with no legal right to do so.

- Potential future de facto control:

- This would exist where, although the DP enjoyed no current legal right of ownership or control, the DP had the legal means to obtain ownership or control.

- Potential future de jure control:

- This would exist where, although there was no evidence that the putative controller was currently exercising de facto control, there is some good reason to believe that the putative controller could, if they wished, exercise control in some manner.

4 TIER TEST AND UBO/BO ASSESSMENTS AND DE JURE AND DE FACTO ROUTES TO CONTROL.

Here’s a clear, concise, and practical explanation of the difference between de jure control and de facto control, especially useful in regulatory, corporate governance, and AML/CFT/SANCTION contexts:

- De jure control (“legal control”) - De jure = “by law.”

- This control exists because the law, a contract, or official documentation explicitly grants a person or entity the right to control a company.

- Examples of de jure control

- Owning more than 50% of voting shares.

- Having the legal right to appoint or remove the majority of directors.

- Control is defined in a shareholder agreement.

- Rights granted through constitutional documents (e.g., Articles of Association).

- Key feature: It is formal, documented, and legally recognised.

- De facto control (“practical control”) - De facto = “in fact” or “in practice.”

- This control exists in reality, even if the person does not have legal or documented authority.

- Examples of de facto control

- Someone who consistently influences decisions because the board follows their recommendations.

- A minority shareholder who has dominant influence due to the fragmentation of other shareholders.

- A founder who retains operational authority despite not holding majority shares.

- A person who provides critical financing and therefore controls major decisions.

- A “shadow director” who directs the board without official appointment.

- Key feature: practical, behavioural, and based on influence, not legal rights.

WHY REGULATORS CARE ABOUT BOTH

AML/CFT, corporate governance, and trust/companies’ regulations (including JFSC, FIU Mauritius, FCA, etc.) insist on assessing both because:

- Criminals often avoid de jure control to conceal ownership.

- They instead exert de facto control, influencing decisions without appearing on official records.

THE PROBLEM

The above typology of control set out by Mr Justice Thompsell [footnote 2]

- Offers a structured legal framework for assessing control in the context of financial sanctions.

- However, HMG recognises that real-world arrangements can be complex and that the facts of a case may not always align precisely with these categories.

This ambiguity results in several practical problems:

- Increased Compliance Costs and Legal Risks:

- Businesses must conduct extensive investigations to assess hypothetical control, which raises operational expenses and exposes them to potential legal liabilities if interpretations are incorrect.

- De-Risking Behaviours:

- To avoid risks, companies may overly cautiously avoid legitimate transactions or relationships, leading to "de-risking" (e.g., withdrawing from markets or clients perceived as risky, even if not actually sanctioned). This can harm innocent parties and disrupt trade, while potentially allowing sanctioned actors to evade restrictions through complex structures.

- Inadequate Legal Concepts and Typologies:

- Existing guidance on control (e.g., typologies like board influence, funding control, or family ties) may not be comprehensive or helpful enough for real-world scenarios, making consistent application difficult across industries.

Purpose of the Consultation

- OFSI's call for evidence, open until 13 April 2026, aims to gather input from industry stakeholders (e.g., financial institutions, legal firms, and businesses) on these challenges.

- The goal is to evaluate whether the current test strikes the right balance: maintaining tough enforcement against sanctioned targets while ensuring regulations are workable and do not unduly hinder legitimate economic activity.

- Responses will inform potential reforms to make the test clearer, more effective, and proportionate, possibly through updated guidance, legal definitions, or examples.

Key Areas for Evidence Sought

OFSI is specifically asking for views on:

- How often does hypothetical control arise in actual cases?

- Its impacts on business decisions, costs, and risks.

- The usefulness of current legal concepts and control typologies in applying the regulations.

This consultation is part of OFSI's broader effort to refine sanctions implementation, ensuring the UK regime remains robust and practical in a complex global environment. For training, emphasise the importance of monitoring such developments, as changes could affect due diligence processes and compliance strategies.

FOOTNOTES

- Mr Justice Thompsell refers here to Mints & Ors v PJSC National Bank Trust - https://www.judiciary.uk/wp-content/uploads/2023/10/Mints-v-PJSC-judgment-061023.pdf↩

- Hellard & Ors v OJSC Rossiysky Kredit Bank & Ors [2024] EWHC 1783 (Ch)

Source

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.