JFSC Money laundering and terrorist financing risk data 2019 - 2023 analysis - INVESTMENT BUSINESS

01/01/2025

In December 2024, the JFSC published some Money laundering and terrorist financing risk data [2019 – 2023], for the following sectors for the first time.

- BANKING

- TRUST COMPANY BUSINESS

- LEGAL

- INVESTMENT BUSINESS - [SEE BELOW]

The data in the reports covers 2019 - 2023 and provides.

- A general overview of each sector along with trends on inherent risk factors such as customers from higher risk jurisdictions and politically exposed persons (PEP) connections.

- An explanation has been provided to support the aggregated data presented through a combination of graphs and tables.

KEY AIMS AND OBJECTIVES

- The aim of publishing these reports is to improve the understanding of money laundering and terrorist financing risk within each sector and enable a comparison across different sectors and activities.

- Key risk indicators are included for each sector to provide useful benchmarking for supervised persons looking to assess their own money laundering and terrorist financing risks.

- The JFSC will be engaging with industry through trade bodies and associations during Q1 2025 to gather feedback and inform future publications.

WARNINGS

- The reports are not risk assessments.

- Whilst some data quality and integrity checks are performed on receipt of the data, the JFSC rely on the accuracy and completeness of data provided by industry.

INVESTMENT BUSINESS SECTOR

- The activity of investment business (IB) is undertaken by a diverse range of businesses, including:-

- Local independent financial advisers (IFAs),

- Niche wealth managers and

- Banks with a global presence.

- IB is divided into 5 “classes” A, B, C, D and E:-

- With this reporting focusing on classes A – D,

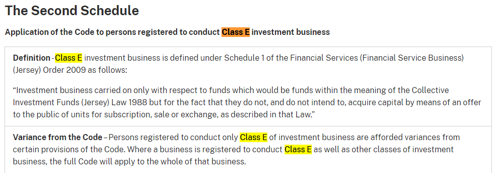

- Class E being rarely used. [Persons registered to conduct Class E investment business are permitted to enjoy amended requirements in respect of certain sections of the Code, as set out in the Second Schedule]

- These include:-

- Dealing in investments (Class A),

- Managing investments (Class B),

- Giving investment advice when not prevented from holding client (Class C) and

- Giving investment advice when prevented from holding client assets (Class D).

- Over the period 2019 to 2023 the value of total assets under administration (or equivalent measure) peaked in 2021 but has generally grown with the total assets under administration, in custody, managed or advised increasing from:-

- £121bn in 2019 to

- £137bn in 2023.

- This includes significant growth in the value of assets advised by Class D entities, which have increased from:-

- £3.9bn in 2019 to

- £11.3bn in 2023.

- Over the same period, the number of firms has declined due to a combination of banks ceasing to operate in Jersey as well as consolidation of non-bank IBs within the sector.

- Much of the data analysed has been split between banks which provide IB services and non-bank IBs. This demonstrates that, in general, banks have a greater proportion of customers from

- Higher risk jurisdictions,

- More connections to politically exposed persons and

- Consider their customers to be higher risk for ML/TF.

- This increased inherent risk may be partially mitigated by the heightened levels of enhanced CDD applied to banks’ IB customers in comparison to non-bank IBs.

Read the JFSC data report for the investment business sector. https://www.jerseyfsc.org/media/7980/sector-data-ib.pdf

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.