JFSC “SUSTAINABLE FINANCE” CONSULTATION - COMMON SENSE PREVAILS

24/09/2025

The JFSC has published feedback on its sustainable finance consultation, and it appears that common sense has prevailed, with the JFSC taking into account the consultation input.

The two key outcomes are as follows.

- SUSTAINABILITY-RELATED RISKS:

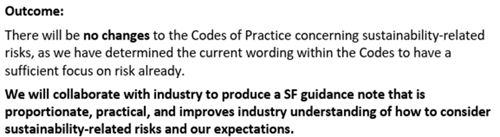

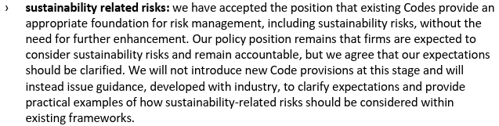

- The JFSC WILL NOT introduce new Code provisions at this stage and will instead issue guidance, developed with industry, to clarify expectations and provide practical examples of how sustainability-related risks should be considered within existing frameworks.

- The JFSC have accepted the position that existing Codes provide an appropriate foundation for risk management, including sustainability risks, without the need for further enhancement.

- The JFSC's policy position remains that firms are expected to consider sustainability risks and remain accountable; however, the JFSC agrees that its expectations should be clarified.

- BUSINESS INTEGRITY RISKS:

- The JFSC will proceed with enhancements to the Codes of Practice (principle 7), including requiring sustainability-related claims to be supported by robust evidence.

- This will bring closer alignment with the FCA’s approach, helping to reflect the desire for consistency across group structures.

- Following registered persons' feedback, the JFSC will:

- Publish a sustainable finance guidance note

- Sustainable finance guidance notes, covering sustainability-related risks and business integrity risks, will be published in Q1 2026.

- Revise Code provisions on anti-greenwashing

- Revised Code provisions on anti-greenwashing will follow a one-year transition period, with full implementation by Q1 2027.

- Publish a sustainable finance guidance note

- To support this process and ensure the guidance meets the needs of the JFSC's local finance industry, the JFSC will work with registered persons on its development before publication and the commencement of the transition period.

Read the JFSC industry update for more information: https://bit.ly/4pyymdn.

THE JFSC SUSTAINABLE FINANCE CONSULTATION FEEDBACK

- On 27 May 2025, the JFSC issued the JFSC consultation on proposals regarding sustainable finance, making proposals in relation to two of the JFSC's lead actions in Jersey’s Sustainable Finance Action Plan.

- The JFSC asked registered persons for feedback on the JFSC's proposed enhancements to the Codes of Practice and notes relating to:

- Integration of sustainability-related risks into governance, risk management and internal systems and controls

- Enhancement of anti-greenwashing measures to ensure sustainability-related claims are fair, transparent and substantiated

- The JFSC said

- There was strong support for the proposed Code enhancements in relation to business integrity risks (anti-greenwashing).

- Feedback also acknowledged that the Codes already place a clear obligation on firms to manage risks.

- Still, there was a clear desire for a greater understanding of the JFSC's expectations on sustainability within the existing framework. Guidance allows us to explain this more clearly and practically.

Feedback on proposals regarding sustainable finance Issued: 24 September 2025

- Feedback on proposals regarding sustainable finance https://www.jerseyfsc.org/media/jc0phag1/feedback-paper-on-proposals-regarding-sustainable-finance.pdf

Executive summary

Introduction

- This paper summarises the feedback received from stakeholders. It provides the JFSC response to the JFSC consultation on proposals regarding sustainable finance (jerseyfsc.org) (CP) published on 27 May 2025.

- The CP focused on two key areas of Jersey’s sustainable finance (SF) framework:

- Integration of sustainability-related risks into governance, risk management and internal systems and controls

- Enhancement of anti-greenwashing measures to ensure sustainability-related claims are fair, transparent and substantiated

Background

- The CP emphasised the importance of advancing the actions set out in the Government of Jersey’s Sustainable Finance Action Plan. It proposed the next steps for registered persons governed by the Codes of Practice to address emerging challenges in SF.

- Building on the anti-greenwashing requirements for sustainable investments introduced in 2021, the CP posed five questions related to proposals for incorporating sustainability-related risks and business integrity risks into the JFSC regulatory framework.

- It aimed to gather views from industry stakeholders on the potential impact that the proposed changes to the Codes of Practice might have on the sectors affected.

- The JFSC received 20 formal responses to the CP from a diverse group of stakeholders, including supervised entities across various financial services sectors, industry associations, professional services firms, and sustainability consultants.

- In addition, 23 people attended and shared their views directly at the JFSC's three drop-in sessions.

- The JFSC is grateful to everyone who took the time to submit responses and participate in the sessions, as well as to Jersey Finance for hosting and arranging the engagements.

International context

- The international conversation on SF is rapidly evolving, even in the short period since The JFSC CP was published.

- Globally, governments and regulators are recalibrating their approach, aiming to balance advancing sustainability objectives and pursuing growth and competitiveness goals. For example,

- The European Union has proposed simplifying reporting under the Corporate Sustainability Reporting Directive (CSRD), reducing the number of companies in scope.

- The United Kingdom is developing its own Sustainability Disclosure Standards, based on the International Sustainability Standards Board (ISSB) framework, with a focus on climate transition planning and assurance.

- The United States, the Securities and Exchange Commission has withdrawn its defence of climate disclosure rules, creating uncertainty around future requirements.

- These developments reinforce the need for Jersey to adopt a pragmatic and proportionate approach to SF, ensuring the industry is provided with support and guidance to identify and mitigate its sustainability-related risks in a way that is not unduly burdensome and enables Jersey to remain competitive.

THE JFSC Feedback summary

The core themes arising from the feedback received were:

- Policy intent: There was broad support for the JFSC SF policy intent, but differing views on implementation.

- The increasing cost of compliance was cited as a negative impact, including the potentially disproportionate impact on smaller firms.

- It was acknowledged that it is essential to progress SF objectives in a manner that is suitable for Jersey.

- Responses were divided on whether the proposals enhanced or hindered competitiveness.

- Codes versus guidance approach:

- Many respondents felt that the current Code requirements for risk management already provided the basis for us to require sustainability risks to be addressed.

- Referring to sustainability specifically was therefore considered unnecessary and potentially detrimental to other risks posed to the industry.

- Almost everyone supported the need for further guidance to clarify the JFSC's expectations regarding sustainability risk.

- Defining terms:

- There was a consensus requesting clear definitions of terms such as ‘sustainability risk’, ‘materiality’ and ‘proportionality’ to support the consistent application of the proposed changes.

- De minimis exemption:

- The majority of respondents opposed a de minimis exemption, citing risks of creating a ‘two-tier’ system and reputational harm.

- Instead, there was support for an emphasis on a proportionate approach to implementation.

- Business integrity risks:

- There was strong support for strengthening requirements in line with international standards.

- Suggestions were made to replace the word “credible” with “robust” evidence, which aligns with UK FCA terminology and mitigates the implication of perceived truth with the use of the word credible.

Policy position and next steps

- The JFSC

- Has carefully considered the responses received, recognising that various perspectives are held within the industry on Jersey’s approach to SF.

- Is committed to the island’s Sustainable Finance Action Plan and playing its part in ensuring the future-proofing of the financial services industry.

- Policy intent remains the same. However, the feedback the JFSC have received has led us to adjust the method of implementation, ensuring it remains proportionate and pragmatic for the island.

- The following outlines the JFSC policy response and next steps:

- SUSTAINABILITY-RELATED RISKS:

- The JFSC have accepted the position that existing Codes provide an appropriate foundation for risk management, including sustainability risks, without the need for further enhancement.

- The JFSC's policy position remains that firms are expected to consider sustainability risks and remain accountable; however, the JFSC agrees that its expectations should be clarified.

- The JFSC will not introduce new Code provisions at this stage and will instead issue guidance, developed with industry, to clarify expectations and provide practical examples of how sustainability-related risks should be considered within existing frameworks.

- The JFSC have accepted the position that existing Codes provide an appropriate foundation for risk management, including sustainability risks, without the need for further enhancement.

- BUSINESS INTEGRITY RISKS:

- The JFSC will proceed with enhancements to the Codes of Practice (principle 7), including requiring sustainability-related claims to be supported by robust evidence.

- This will bring closer alignment with the FCA’s approach, helping to reflect the desire for consistency across group structures.

- SUSTAINABILITY-RELATED RISKS:

- 2026 -2027

- A Sustainable Finance guidance note, covering sustainability-related risks and business integrity risks, will be published in the first quarter of 2026.

- Revised Code provisions on anti-greenwashing will follow a one-year transition period, with full implementation by the first quarter of 2027.

- To support this process and ensure the guidance meets the needs of local industry, the JFSC will work with industry on its development before publication and the start of the transition period.

Read the JFSC's full feedback paper on proposals regarding sustainable finance.

The Team

Meet the team of industry experts behind Comsure

Find out moreLatest News

Keep up to date with the very latest news from Comsure

Find out moreGallery

View our latest imagery from our news and work

Find out moreContact

Think we can help you and your business? Chat to us today

Get In TouchNews Disclaimer

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.

As well as owning and publishing Comsure's copyrighted works, Comsure wishes to use the copyright-protected works of others. To do so, Comsure is applying for exemptions in the UK copyright law. There are certain very specific situations where Comsure is permitted to do so without seeking permission from the owner. These exemptions are in the copyright sections of the Copyright, Designs and Patents Act 1988 (as amended)[www.gov.UK/government/publications/copyright-acts-and-related-laws]. Many situations allow for Comsure to apply for exemptions. These include 1] Non-commercial research and private study, 2] Criticism, review and reporting of current events, 3] the copying of works in any medium as long as the use is to illustrate a point. 4] no posting is for commercial purposes [payment]. (for a full list of exemptions, please read here www.gov.uk/guidance/exceptions-to-copyright]. Concerning the exceptions, Comsure will acknowledge the work of the source author by providing a link to the source material. Comsure claims no ownership of non-Comsure content. The non-Comsure articles posted on the Comsure website are deemed important, relevant, and newsworthy to a Comsure audience (e.g. regulated financial services and professional firms [DNFSBs]). Comsure does not wish to take any credit for the publication, and the publication can be read in full in its original form if you click the articles link that always accompanies the news item. Also, Comsure does not seek any payment for highlighting these important articles. If you want any article removed, Comsure will automatically do so on a reasonable request if you email info@comsuregroup.com.